Major US carriers will account on Wednesday for the $54 billion payroll assistance package awarded by the government to the struggling sector during the Covid-19 pandemic.

According to Reuters, the Senate Commerce Committee will hear from the chief executives of American Airlines, Southwest Airlines, and United Airlines, as well as the chief of operations of Delta Air Lines and the head of a large flight attendant union. Others, such as JetBlue Airways and Alaska Air Group, will submit written statements.

The committee chair, Senator Maria Cantwell, urged airline CEOs to participate in the oversight hearing after she sent them letters about reports of staff shortages, significant flight cancelations and delays.

Lawmakers are expected to question executives about how the airlines have used pandemic-related federal rescue funds, as well as about personnel issues, among other matters.

Read more

American & United axing 32,000 jobs as government cannot agree on airline bailout

Since March 2020, Congress has awarded major US airlines a collective total of $54 billion in order to keep thousands of workers on the payroll for 18 months. Of that funding, the airlines must together repay $14 billion, and the US Treasury currently has warrants worth about $200 million, according to a Commerce Committee memo. The Treasury has also provided $25 billion in low-cost loans to airlines.

Airlines that have accepted government aid to fund payrolls until September 30 were barred from taking time off or firing employees, and faced caps on executive pay and a ban on share buybacks and dividends.

According to the trade association and lobbying group Airlines for America, without the help, “airlines would undoubtedly have reduced capacity in proportion to the drop in passenger traffic to avoid a sharp drop in load factors.” The association told the committee that “about 50,000 airline employees have opted for early retirement or voluntary separation.”

US air passenger travel plunged 60% last year, to its lowest level since 1984. Airlines say the coronavirus is causing a drag on demand to sub-2019 levels.

“The Omicron variant has created even more uncertainty, and there is no clear consensus on when corporate and international travel will return,” said Delta’s chief of operations John Laughter.

For more stories on economy & finance visit RT’s business section

Social media platform Reddit announced it has confidentially filed a draft registration with the US Securities and Exchange Commission (SEC) to become a publicly traded stock.

“The initial public offering is expected to occur after the SEC completes its review process, subject to market and other conditions,” Reddit Inc. said in a statement released on Wednesday.

According to the company, neither the number of shares that would be offered nor the price range for the stock have been determined so far.

Read more

AMC stock soars over 20% as Reddit-fueled rally extends to another week

Reddit hoped to be valued at more than $15 billion, according to unnamed sources cited by Reuters back in September, shortly after the company was valued at $10 billion in a private fundraising that brought around $700 million. In February, Reddit raised another $250 million.

Reddit was founded in 2005 by Steve Huffman and entrepreneur Alexis Ohanian. It became known for its niche discussion groups, lagging in popularity of other major social media platforms like Facebook or Twitter. In 2006, the platform was purchased by global mass media company Conde Nast. Reddit became an independent subsidiary a decade ago.

The enormous media influence of the platform came to light in January 2021. An army of stay-at-home traders, communicating on Reddit’s WallStreetBets forum, rocked Wall Street by betting against hedge fund short positions on a number of companies.

They bet on shorted stocks like GameStop and AMC. As a result, stocks of the struggling brick-and-mortar video game retailer and theater chain skyrocketed, costing hedge funds billions.

For more stories on economy & finance visit RT’s business section

A senior official at the Bank of England has questioned the value of Bitcoin, which soared to $68,000 last month, citing the currency’s volatility and warning that digital assets could theoretically or practically drop to zero.

According to Deputy Governor Sir Jon Cunliffe, fast-growing digital assets could pose a danger to the established financial system.

Read more

Crypto platform glitch briefly makes traders trillionaires

In an interview with the BBC, Cunliffe said that at present around 0.1% of British households’ wealth was held in cryptocurrencies. And, if their value was to fall sharply, it could have a knock-on effect.

Cryptocurrencies are “growing very fast,” he explained, and are being integrated into the financial system; a significant change in price could affect other markets and established financial players.

“It’s not there yet, but it takes time to design standards and regulations,” Cunliffe added.

Not everyone shares Cunliffe’s grim outlook. After reaching peak price in November, Bitcoin dropped back below $46,000 early this month. However, many experts believe the asset is on its way to passing the $100,000 mark. Bloomberg predicted earlier this year that Bitcoin could rise as high as $400,000 by the end of 2021.

For more stories on economy & finance visit RT’s business section

Wednesday evening was marked by another bold statement from Tesla CEO Elon Musk on Twitter. The billionaire entrepreneur claims that he will pay more taxes this year than any other American in history.

The tweet came as part of his spat with Senator Elizabeth Warren (D-Massachusetts), who has been a longtime supporter of wealth tax that would target not only the income of the richest US citizens, but their assets as well.

“And if you opened your eyes for 2 seconds, you would realize I will pay more taxes than any American in history this year,” Musk tweeted in response to Warren’s reaction to the fact that TIME magazine named him its “Person of the Year.”

Read more

Musk fires back at ‘Senator Karen’ over tax tweet

“Let’s change the rigged tax code so The Person of the Year will actually pay taxes and stop freeloading off everyone else,” Warren tweeted.

The eccentric billionaire responded by calling the politician a “Senator Karen” in one of his follow-up tweets.

“You remind me of when I was a kid and my friend’s angry Mom would just randomly yell at everyone for no reason,” Musk said. “Please don’t call the manager on me, Senator Karen.”

The term “Karen” has been widely used in America as a slang word to refer to white women perceived as entitled or demanding.

Warren’s claims about Musk not paying much in taxes aren’t entirely baseless. According to a ProPublica investigation published in 2018, Musk paid nothing in federal income taxes that year. The billionaire reportedly paid less than $70,000 in taxes back in 2015 and 2017.

However, Musk, who currently doesn’t earn a cash salary, but only owns stock in his companies, likely owes the federal government at least $8.3 billion for 2021, according to Forbes’ estimates. The figure is reportedly based on the stock sales of nearly $13 billion the world’s richest person implemented through December 13.

For more stories on economy & finance visit RT’s business section

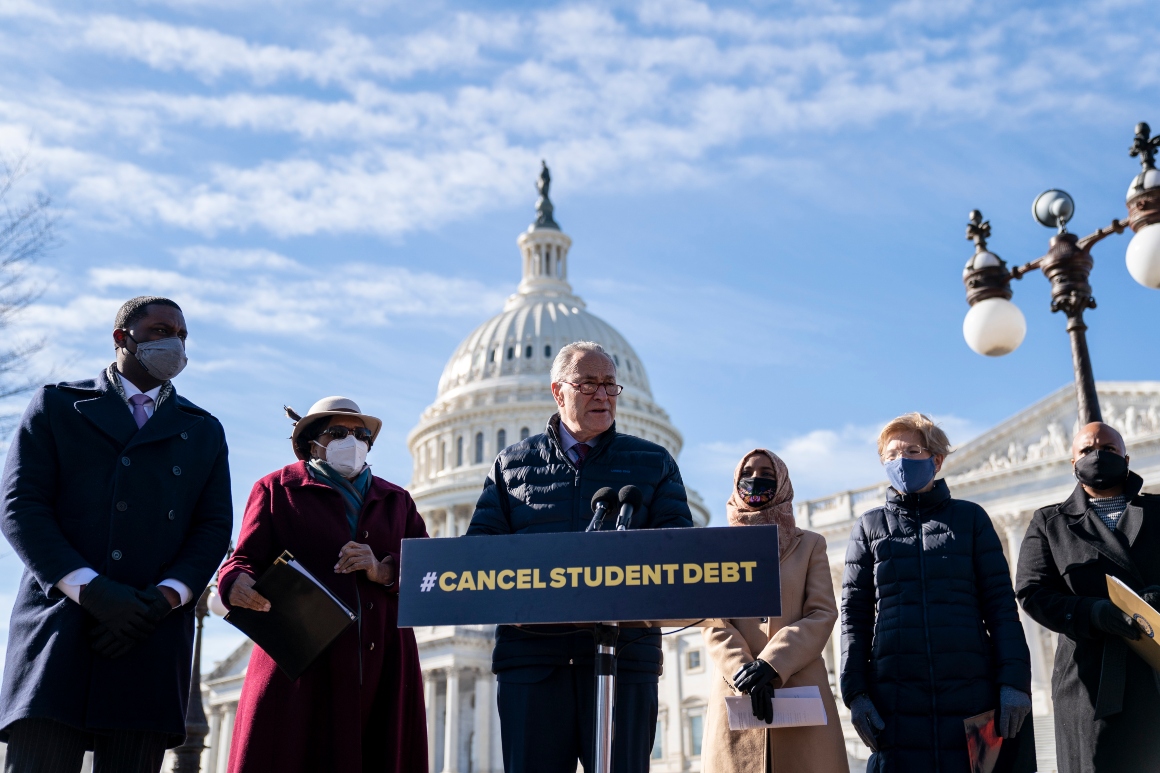

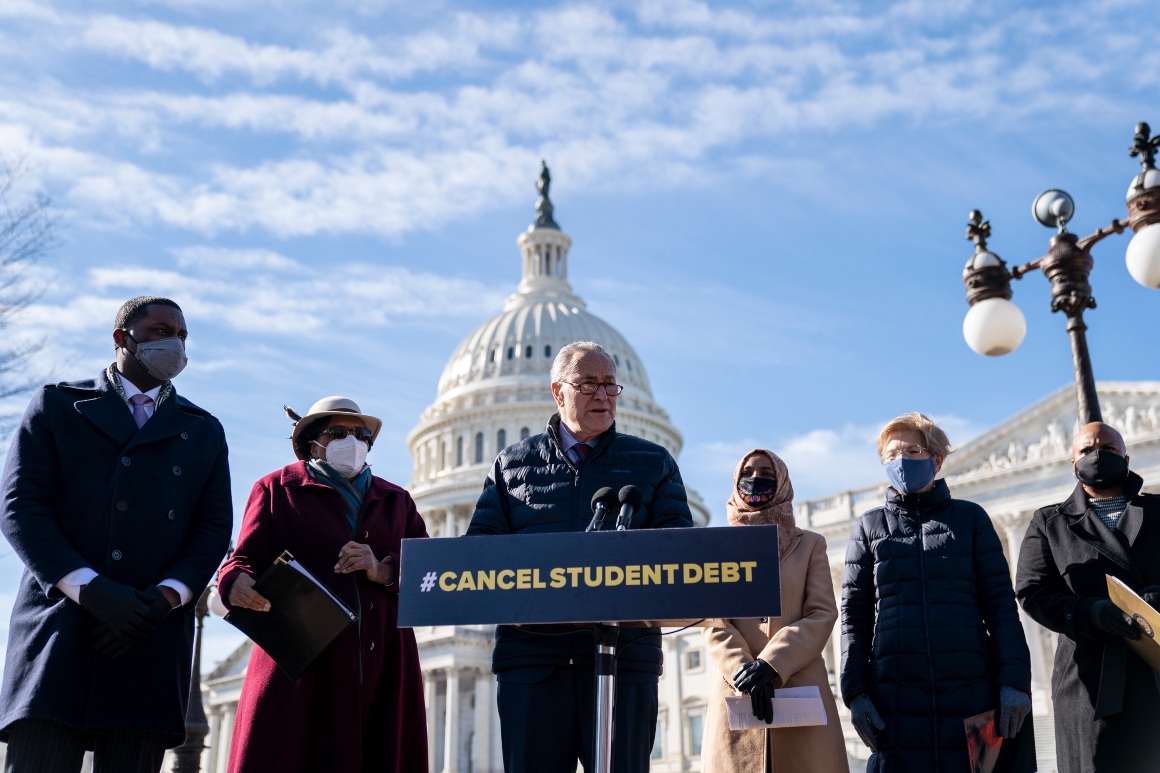

Top Democrats are urging the Biden administration to again extend the freeze on federal student loan payments before it expires next month, warning that requiring tens of millions of Americans to resume paying their debt will drag down the economic recovery.

Monthly student loan payments and interest are set to resume on Feb. 1 for the first time since the beginning of the pandemic when the federal government took emergency action to freeze the debt as the economy cratered in March 2020.

Majority Leader Chuck Schumer, Sen. Elizabeth Warren (D-Mass.) and Rep. Ayanna Pressley (D-Mass.), who for months have been urging President Joe Biden to cancel large amounts of outstanding student loan debt, are asking the administration to further extend the payment pause.

At a minimum, the lawmakers said in a letter this month to Biden, the administration should continue the freeze on student loans “until the economy reaches pre-pandemic employment levels.”

The lawmakers also released a new analysis by the progressive Roosevelt Institute, which estimates that some 18 million American families would have to collectively pay more than $85 billion next year if the Biden administration restarts payments as scheduled.

Those payments would “hurt individual families and the economy as a whole,” the lawmakers wrote to Biden, adding that the emergence of the Omicron “variant is a reminder the virus is still impacting parts of the economy and public health.”

White House press secretary Jen Psaki said Friday that the administration would release more details about its plans in the coming weeks and is “preparing for a range of steps” ahead of the Feb. 1 expiration.

“We’re still assessing the impact of the Omicron variant,” she said. “But a smooth transition back into repayment is a high priority for the administration.”

Mounting pressure for an extension: The letter comes amid growing calls on the left for the Biden administration to continue the relief for borrowers as the White House decides the broader question of whether to outright cancel student loan debt, which it has publicly said it continues to review.

A wide coalition of mostly left-leaning organizations, consumer advocacy groups and unions last week also called on the Biden administration to extend the payment pause.

The groups, led by the Student Borrower Protection Center, said in a letter to the White House that “a rush to resume student loan payments is a recipe for disaster and will result in widespread confusion and distress for student loan borrowers.”

Earlier last week, Sens. Raphael Warnock (D-Ga.) and Ron Wyden (D-Ore.) led a dozen other Senate Democrats in urging the Biden administration to at least continue to keep the interest rates on federal student loans at zero even if monthly payments resume on Feb. 1.

The Education Department has estimated that the waiver of interest on federal student loans alone saves borrowers about $5 billion each month.

Key context: Biden administration officials at the Education Department have repeatedly said they’re planning to resume the collection of student loans in February — for the first time in nearly two years.

Congress in March 2020 suspended monthly payments and interest on most types of federal student loans, and the Trump and Biden administrations have each used executive action to continue that relief.

The Education Department announced the most recent extension of the relief in August. Some White House officials at the time had been reluctant to issue that extension, which top Education Department officials had recommended, because of concerns that continuing the emergency program would undercut the administration’s messaging about the strength of the economic recovery.

The Education Department has already begun sending emails to borrowers reminding them that payments will resume in February. Department officials and their contracted loan servicing companies have been working to implement some new flexibilities for borrowers as they return to repayment next year.

Biden administration officials have said they are continuing to review proposals for a mass student debt jubilee. But in the meantime they’re focused on improving existing student debt relief programs targeted at specific populations of borrowers, such as public service workers or those with severe disabilities.

The Education Department has touted roughly $12 billion in student debt that has been forgiven under those existing federal programs since the beginning of the Biden administration.